Capital is primarily moved through traditional finance, which has controlled the transfer for over 100 years. Geographic gatekeepers are one reason for the slow speed of capital exchange; ownership records exist in paper form rather than digitally, thus making the settlement process very slow and costly compared to RWA tokenization methods. The traditional financial system will continue to have these issues until RWA tokenization becomes a viable option for all assets on a global scale. In five years (2026), there should be a significant number of institutions issuing real tokenized projects based on RWA tokenization.

According to an RWA.xyz report, there are currently over 24 billion dollars worth of total value locked (TVL) in the on-chain tokenized asset market. With this development, there are now clear (measurable), credible (verifiable), and large (financially) differences between the existing traditional financial infrastructure versus the emerging blockchain infrastructure supporting RWA tokenization.

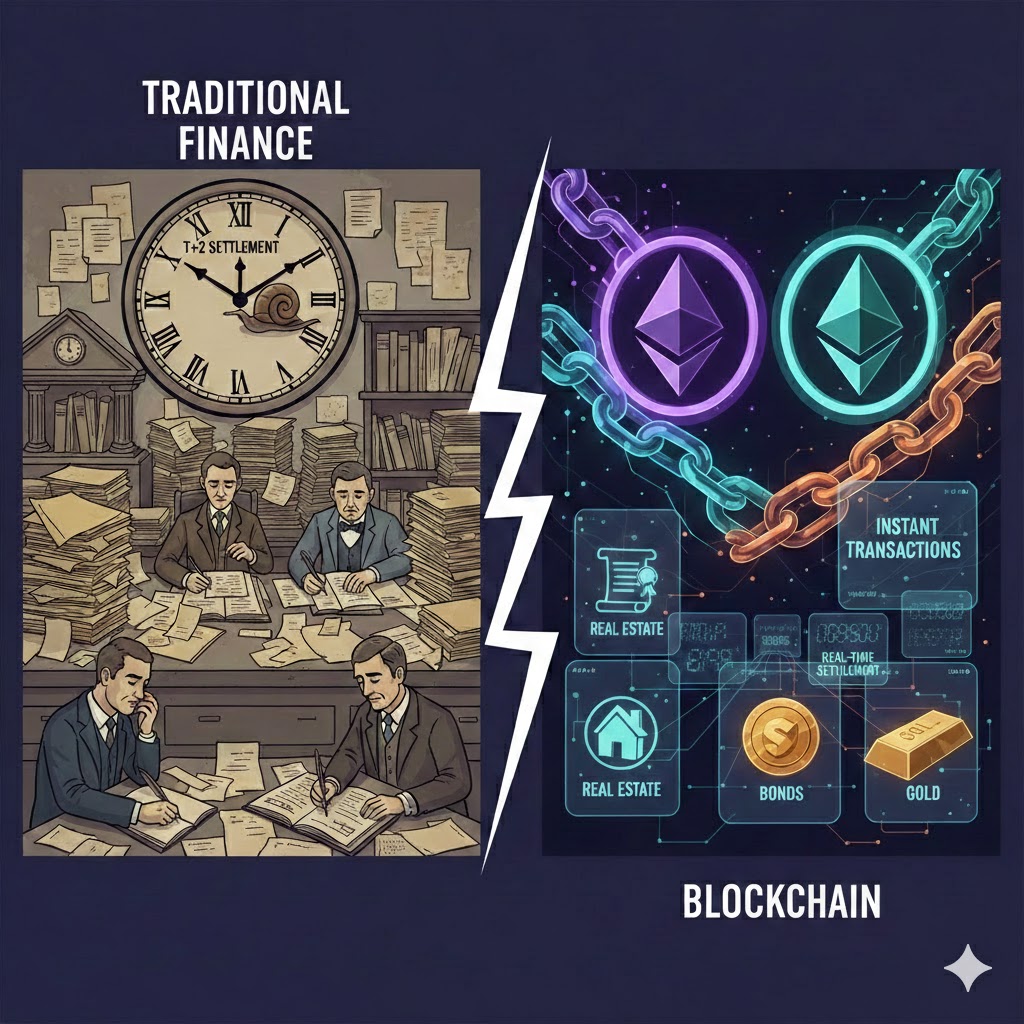

Settlement Speed: T+2 vs Near-Instant On-Chain Finality

When someone purchases a bond, stock, or real property in traditional finance, the transfer of ownership does not occur immediately. If a person purchases private debt or real estate (products that are more complex), the settlement process typically takes several weeks or even months due to the involvement of attorneys, custodians, clearinghouses, and registrars throughout the settlements process. The average time it takes for a trade to settle is called T+2, which is two business days after the date of the trade. The simple transfer of ownership from one party to another is complicated by the cost, time, and counterparty risk that each intermediary introduces. Today, even though markets have moved to a fully digital nature, they have yet to find a way to overcome the former physical limitations of all of the manual reconciliations and the 'paper' records that were previously used.

With the assistance of an on-chain RWA resolution process, structural latency has been entirely eliminated from the process of transferring and recording ownership. Instead of taking days to transfer assets using a paper-based system, the use of Ethereum's smart contracts allows an ownership record to be updated and transferred in just minutes and for this updated ownership record to be verified in real-time using a standard Ethereum blockchain block. In addition to the Ethereum benefits of real-time verification of ownership updates happening in minutes rather than days, Solana provides an even greater advantage in terms of velocity of asset movement through its use of high-frequency transaction processing.

This high-frequency transaction processing allows a transaction to occur every 400 milliseconds on average and costs less than $0.01. The need for instant capital efficiency and speed was demonstrated by JPMorgan's ability to transfer tokenized collateral in real-time using the blockchain to satisfy margin calls that, if transacted using traditional means, would have taken hours to complete. As a result, all parties involved in the transaction will benefit from capital efficiency as the settlement of a transaction is essentially instantaneous and is ongoing.

Market Hours: Business Days vs 24/7 Blockchain Markets

Traditional financial systems operate on schedules that go back before the invention of computers. The U.S. stock exchange operates from 9:30 AM to 4 PM ET, Monday to Friday. The times for bond markets, registration of real estate, and private credit facilities are the same and limit access to the financial system during weekends and holidays. So if you live in Southeast Asia and want to react to a stock market event at 2:00 AM, you can't because you are locked out of the system. Due to this fact, there have been no changes to the basic structure of the traditional financial systems that have been created around this old system of keeping the time of processing of transactions.

This limitation is not a characteristic of the financial system.

Since technology never sleeps, neither do blockchain-based markets. For example, Ondo Finance's OUSG and other tokenized Treasury securities earn yield every day (including weekends). PAXG and XAUT tokenized gold can be traded through DeFi protocols around the clock. Without requiring an intermediary or human operator, smart contracts can enable income distributions, margin calls and collateral moves at any hour of the day. Tokenized RWAs offer crypto players the same 24/7 access to asset classes as traditional finance did beyond office hours. For that reason, the expectation of 24/7 service has already been established in the crypto community.

Access and Minimum Investment: Accreditation vs Fractional On-Chain Ownership

The hurdles imposed by traditional finance on private credit funds, hedge funds, and many institutional bond offerings are true "accreditation" barriers - meaning an investor is considered "accredited" after either having at least $1M in net worth or $200K in annual income in the US. Therefore, to make an invested equity stake in commercial real estate involves a minimum commitment (usually in the hundreds of thousands) while providing a very low-yield option for retail investors that otherwise would be accessing some of the highest-quality assets.

These are set thresholds and can restrict access to certain "lowest-cost" assets for individuals and organizations of wealth and capital. They also artificially distribute wealth over generations.

These minimums break down at the infrastructure level into RWA tokenization. For instance, Tokenization of a $10 million commercial real estate can allow for fractional ownership. This creates an opportunity for tokenizing investors to purchase entry points (tokens) at a low cost ($50 in this case). As demonstrated by a number of platforms such as RealT, rental income is distributed daily to all token holders in the form of stablecoin. Government-backed yield via Ondo Finance's tokenized Treasury products will be available to anyone who meets the basic onboarding requirements for tokenized assets, without the limitations of capital on the traditional finance side. This reduction in the minimum investment qualification enables greater eligibility to participate in wealth-generating asset classes, so Deloitte's Center for Financial Services forecasts over $1 trillion of tokenized real estate by 2035.

Transparency and Auditability: Quarterly Reports vs Real-Time On-Chain Verification

Standard banking furnishes inadequate levels of openness and accountability as many investors exclusively rely on audited financial statements and the information provided in quarterly and annual regulatory filings. The information provided by the asset manager or fund manager is typically controlled by the asset manager or fund manager, and therefore structural limitations are associated with the limited availability of information (since there is not a universal standard) include, but are not limited to, fraud and deception; selective disclosure. By the time an investor receives the regulatory filing, they are typically unaware of material developments or declines in performance (for example, the distress associated with a fund's private credit portfolio) that occurred weeks or months prior to the distribution of the regulatory filing to investors.

The on-chain RWA infrastructure completely flips the relationship between the asset issuers and investors. For instance, using blockchain explorers, anyone can verify an ownership transfer, yield distribution, reserve holding, or compliance activity as documented on the public ledger. Whereas most other asset classes rely on periodic third party audit for auditability, there are by default automated confirmations of the tokenized assets being represented by the real world holdings via Chainlink's Proof of Reserve technology, without needing to wait for a third party audit . As such, this verification process fundamentally reorients the trust paradigm of the asset issuer to the investor, and represents more than just a feature. The use of the verification process instead of trust as the guiding principle throughout the cryptocurrency ecosystem have effectively applied this principle to the asset classes for which opacity has been present.

Programmability: Static Instruments vs Smart Contract Automation

Programmability is probably the key difference between a blockchain-based RWA infrastructure versus traditional finance (TradFi). For example, a typical bond is issued by an issuer, paid by an agent or paying (the middleman), cleared by a custodian, and finally the actual payment transferred to an investor's account, all through multiple intermediaries that take a fee at every step along the way. Bonds pay a predetermined coupon amount on a predetermined date(s), and are static until the next coupon date; there is no possibility of making conditional payments, there is no response to market fluctuations, and they can't communicate with other financial instruments, nor with other bonds in the series.

Programmable financial products consist of tokenized real-world assets that are encoded via smart contracts. They can self-pawn as collateral for DeFi lending protocols without any human involvement, autonomously change for compliance triggers (such as a change in investor KYC status), pay out yield daily instead of quarterly, and can interact with other on-chain assets using composable smart contract calls. Derivatives structures that would require custom legal engineering to run in traditional finance are able to run automatically on-chain, allowing for the separation and trading of the yield component of tokenized Treasury securities (for example, the Pendle Finance yield tokenization protocol). This programmability creates more than just existing financial products. The crypto ecosystem is poised to serve as the foundational infrastructure layer for the next generation of financial innovation and enables entirely new types of financial products that do not exist in traditional finance.